Inventory costs rarely stay still. One month, a product costs ten dollars to buy. A few weeks later, the same product may cost twelve. Shipping, supplier changes, fluctuations in raw materials, and currency shifts all play a part. For an e-commerce store that sells the same item every day, these changes quietly accumulate within the accounting system.

Profit tracking becomes difficult when supply costs fluctuate while sales continue. If you sell identical items bought at different price points, your margins appear inconsistent. The Weighted Average Cost method handles this by combining all purchase prices into one steady average. That value is then used across the full inventory for consistent accounting, allowing e-commerce sellers to keep reliable financial records even when market prices keep shifting.

What Is the Weighted Average Cost Method?

The Weighted Average Cost method, or WAC, values inventory by averaging the cost of every unit available for sale. Under this framework, every product in stock is assigned an identical cost, regardless of whether individual batches were purchased at different market rates.

Rather than tracking each shipment separately, the system calculates the total expenditure for all current stock and divides it by the total quantity on hand. This resulting average becomes the fixed cost used for every item sold and every unit remaining in the warehouse. It simplifies bookkeeping by providing a single, consistent value for financial reporting.

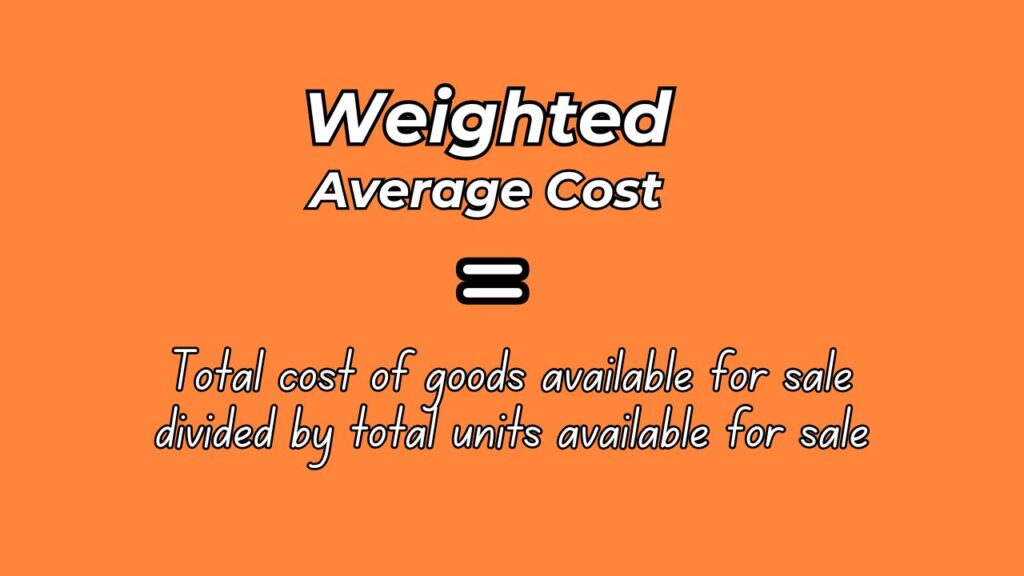

The formula looks like this:

Weighted Average Cost = Total cost of goods available for sale divided by total units available for sale

This method suits companies that move high volumes of the same products. Dropshipping stores, private label sellers, and wholesale operations usually deal with repeating SKUs. Recording each shipment at a separate cost would slow accounting work and increase the chance of mistakes.

Inventory Weighted Average removes that burden. It gives one clean number that updates automatically each time new stock arrives.

How to Calculate WAC With a Step-by-Step Example

A simple example shows how this works in practice.

Imagine an online store buys inventory twice during a month.

- First purchase: 100 units at $5 each

- Second purchase: 100 units at $10 each

The total cost for the first batch is $500.

The total cost for the second batch is $1,000.

Now combine both purchases.

- Total units available for sale: 200

- Total cost of goods available for sale: $1,500

To calculate the weighted average cost:

$1,500 divided by 200 units = $7.50 per unit

That $7.50 becomes the cost used for every sale. It does not matter which physical unit was shipped. The accounting system records $7.50 as Cost of Goods Sold for each item.

If 60 units sell, COGS is $450.

If 150 units sell, COGS is $1,125.

The remaining inventory still carries the same $7.50 value per unit. As new stock arrives, the calculation runs again and updates the average.

This rolling average keeps profit reporting steady and prevents sudden spikes in costs from distorting financial statements.

WAC vs FIFO vs LIFO

Inventory valuation methods respond to changing prices in their own ways. The three approaches most businesses see are WAC, FIFO, and LIFO. Each one shapes reported profit, tax exposure, and balance sheet values. When prices rise, some methods push higher costs into sales while others leave them in stock.

When prices fall, the effect flips. Sellers using imported goods or fast-moving items feel these differences more clearly across monthly reports.

Choosing the right method is less about theory and more about how inventory flows through warehouses and how management wants results to appear over time for planning and review.

FIFO

First In, First Out assumes the oldest stock sells first. Items bought earlier get recorded as COGS before newer inventory. This works well for food, cosmetics, or products with expiration dates. When prices rise, FIFO usually shows higher profits because older, cheaper items are counted as sold first.

LIFO

Last In, First Out assumes the newest stock sells first. This pushes higher recent costs into COGS. In periods of rising prices, profit looks lower. Many accounting standards restrict or block this method.

WAC

Inventory Weighted Average sits between these two. It blends old and new prices. Sudden price jumps get smoothed instead of showing up all at once. The result is a more stable view of margins across time.

For e-commerce stores dealing with overseas suppliers and frequent cost shifts, that stability matters.

| Method | Cost Assumption | Impact When Prices Rise | Best Use Cases | Key Takeaway |

|---|---|---|---|---|

| FIFO | Oldest inventory sells first | Higher reported profit | Perishable or fast-moving goods | Profits look stronger, costs lag |

| LIFO | Newest inventory sells first | Lower reported profit | Inflationary cost environments | Lower taxes, limited acceptance |

| WAC | Average cost of all inventory | More stable margins | E-commerce, imported goods | Smooths cost volatility |

Pros and Cons of the Weighted Average Method

Like any accounting approach, the Inventory Weighted Average method presents specific advantages and practical trade-offs. While it offers a streamlined way to manage fluctuating supply costs, it may not be the perfect fit for every business model or inventory type.

Advantages

The Weighted Average Cost method offers several useful benefits for inventory management:

- Simple Calculation: It can be worked out and updated easily without heavy manual effort.

- Lower Recordkeeping: Needs fewer entries compared to managing each batch on its own.

- Cost Stability: Levels out supplier price changes, creating a steadier cost reference.

- Profit Consistency: Limits sharp swings in reported profit margins over time.

- Software Compatibility: Works smoothly with automated inventory systems for live data updates.

Limitations

While efficient, the WAC method has specific limitations:

- Hides Cost Shifts: It may soften the effect of rising replacement prices, which makes inflation harder to notice right away.

- Reduced Detail: It gives less visibility than recording every purchase on its own, which can matter for expensive products.

- Limited Use: It does not suit items with expiry dates or unique serial codes where batch-level tracking is required.

For most online stores selling standardized goods, these drawbacks are usually minor compared to the time saved.

How NextSmartShip Supports Inventory Weighted Average

Weighted Average Cost only works when inventory data stays accurate. That means every unit received and every unit shipped must be recorded correctly. Gaps or delays throw off the math.

NextSmartShip tracks inventory movements in real time across its fulfillment centers. Each product received is logged with quantity and SKU details. Each order shipped updates stock levels immediately. That creates a live view of how many units are available at any moment.

This live inventory data allows accounting teams to apply the Inventory Weighted Average formula without manual stock checks. The system already knows how many units entered and left the warehouse. That information feeds directly into cost calculations.

Keeping a precise Weighted Average Cost relies on the accuracy of incoming and outgoing data. When inventory records are handled carefully, the following benefits have a direct effect on the bottom line:

- Clear Goods Received Records: Full records for each inbound shipment make sure purchase price changes are captured correctly before being averaged into the system.

- Accurate Goods Shipped Data: Careful tracking of outbound orders avoids stock gaps that could otherwise distort cost calculations.

- Fewer Reconciliation Errors: Strong data quality reduces the need for manual fixes during audits, keeping the system average in line with actual stock.

- Quicker Monthly Close: With organized data updating in real time, accounting teams can finish reports without chasing missing invoices or batch details.

- Improved COGS Accuracy: Trusted inputs produce a more realistic Cost of Goods Sold, supporting better pricing decisions and tax reporting.

When fulfillment data stays reliable, financial reporting follows.

Conclusion

The Weighted Average Cost method gives e-commerce sellers a steady way to view profit. Instead of chasing every price change, it creates one blended cost that reflects what the business actually paid. That makes COGS easier to track and margins easier to understand. Accountants often recommend WAC for stores that sell the same items again and again while dealing with changing supplier prices. It keeps reporting simple and reduces noise inside financial statements.

Accurate inventory data makes the method work. A fulfillment partner that tracks every unit received and shipped gives businesses the clean records needed to apply WAC with confidence. Collaborate with NextSmartShip to maintain sound inventory management and clear accounting across every sales channel.